AI for angel investors is becoming more tempting for one simple reason: pitch flow has become larger than the unaided human mind can responsibly hold.

An active angel investor may receive decks from founders, syndicates, accelerators, warm introductions, cold inbound messages, advisors, and other investors. Some decks are weak. Some are polished but hollow. Some are badly presented but contain a real opportunity. Some look like every other AI startup until one buried detail changes the entire question.

This article is a fictionalized composite case study. It is not investment advice. It is a way to show what happens when a serious investor uses a local deep reasoning LLM to screen fundraising pitches, loses control even with well-designed prompt templates, and then rebuilds the workflow through Adjoint Thinking.

The lesson is not that investors should avoid AI. The lesson is sharper: AI can help an investor see more, but it must not be allowed to decide what matters.

The Investor Before Adjoint Thinking

Maya was an angel investor with a technical background, a strong founder network, and a disciplined thesis. She liked infrastructure software, scientific tools, and products where technical depth created a real moat.

Her problem was not lack of intelligence. It was saturation.

She was seeing too many decks, too many claims, too many market maps, too many traction charts, and too many founder narratives that sounded credible for the first ten minutes. Every pitch required several kinds of attention at once:

- What is the company actually building?

- Is the pain real or just well-described?

- Is the market claim specific enough to matter?

- Is the traction meaningful or vanity-shaped?

- Does the technical advantage survive scrutiny?

- What would have to be true for this to become a fund-returning company?

- What is being hidden by the polish of the deck?

Her first solution was reasonable. She built a local AI workflow.

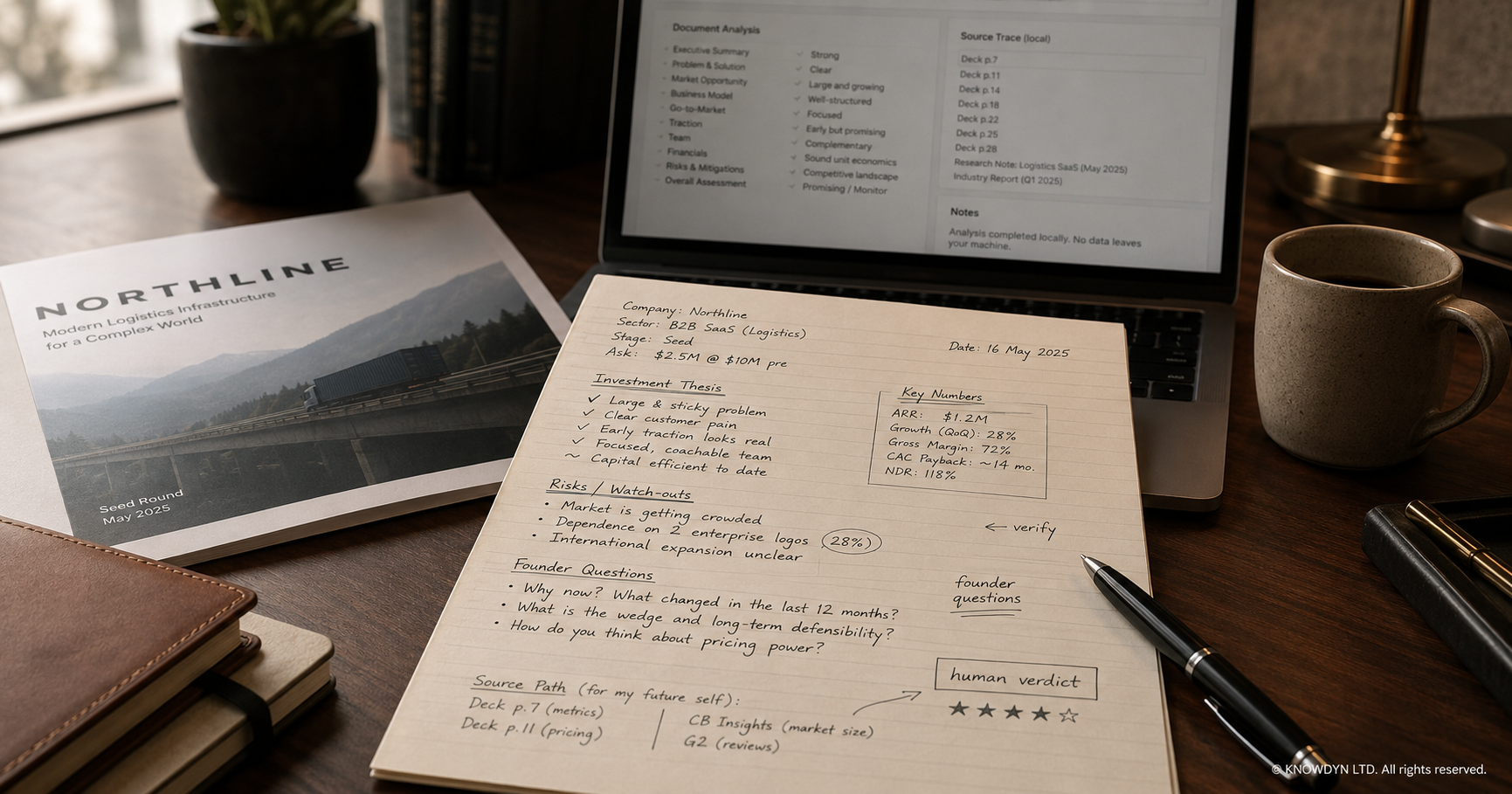

Because many pitch decks are confidential, she used a top-tier deep reasoning LLM running locally in her private environment. The model ingested a deck, extracted the main facts, and reorganized them into her preferred investment structure:

- Company summary

- Founder background

- Customer pain

- Product and technical wedge

- Market category

- Business model

- Evidence of demand

- Competition

- Risks

- Questions for the founder

- Initial investment memo

This gave her speed. A thirty-slide deck became a structured memo in minutes. A messy deck became readable. A polished deck became searchable. She could compare companies more easily and enter founder calls better prepared.

At first, it felt like control.

Then the problem changed.

Why the Prompt Templates Still Failed

Maya did not use lazy prompts. She had built careful multi-shot templates. Each prompt included examples of good extraction, bad extraction, risk flags, due diligence questions, and investment memo structure.

The templates were not bad. They were too successful.

They created outputs that looked like her own thinking before she had actually thought enough.

The model learned her preferred structure so well that every startup began to arrive in the same investment shape. The deck might be weak, but the memo looked disciplined. The market might be vague, but the section headings made it feel analyzable. The founder’s claim might be unsupported, but the AI-generated memo placed it neatly under “traction” or “technical advantage.”

The danger was not crude hallucination. It was structured overconfidence.

The prompt template gave every startup a frame. The frame made weak companies look more comparable than they were. It also made unusual companies look weaker when they resisted the template.

Maya noticed four failures.

1. The Machine Turned Extraction Into Interpretation

The model was supposed to extract information. But extraction quietly became interpretation.

A sentence from the pitch deck such as “we are seeing strong pull from enterprise design partners” became “early enterprise demand is emerging.” That sounded reasonable. But it was not the same claim.

Were these paid pilots? Letters of intent? Friendly advisors? One-off conversations? Existing customers? The deck did not say.

The model had not invented a fact. It had softened an ambiguity into investor language.

2. The Preferred Structure Became a Hidden Verdict

Maya’s template was designed around her investment taste. That seemed like an advantage. But the structure began to behave like a verdict machine.

A startup with a clear technical wedge and weak go-to-market plan looked promising because her framework elevated technical defensibility. A startup with messy technical language but unusually strong customer urgency looked weaker because it did not fit the template as cleanly.

The AI did not decide for her directly. It shaped what became easy to notice.

3. Research Became Conversational Grazing

After the first memo, Maya opened a co-thinking session.

She asked the model to research the market, list competitors, compare pricing, find customer pain signals, challenge the founders’ assumptions, and suggest questions for a call.

Each exchange felt productive. The model produced more angles, more objections, more comparisons, more founder questions, and more possible risks.

But the session began to sprawl.

The more she asked, the less she could tell which claims came from the deck, which came from external research, which came from the model’s inference, and which came from her own prior knowledge.

She had more information, but less command of provenance.

4. The Investment Memo Became Too Smooth

The final memo was beautifully structured. That was the warning sign.

It had a company summary, a market narrative, a risk section, a thesis, a recommendation, and a list of open questions. It looked like something an investor could send to a syndicate.

But Maya began to feel the discomfort that good investors learn not to ignore. The memo had reduced the roughness of the company. It had converted contradictions into “risks,” missing evidence into “questions,” and founder ambition into “strategic opportunity.”

The memo was not obviously wrong.

It was insufficiently wounded by the evidence.

The Shift to Adjoint Thinking

Maya did not abandon AI. She changed the jurisdiction of the machine.

Before Adjoint Thinking, her workflow asked:

“How can I make the LLM produce a better investment memo?”

After Adjoint Thinking, her workflow asked:

“Where exactly should machine assistance touch my investment judgment?”

That question changed everything.

She stopped treating the model as a memo generator. She turned it into a controlled cognitive environment with roles, boundaries, provenance, and verification status.

The machine could still extract. It could still reorganize. It could still challenge. It could still research. But it could no longer collapse extraction, synthesis, research, and judgment into one smooth answer.

The New Workflow

Maya rebuilt her pitch screening process around five Adjoint Thinking moves.

1. She Named the Pressure Before the Prompt

Before uploading a deck, she wrote one sentence:

“What is the pressure of this decision?”

For example:

“This company looks technically strong, but I do not yet know whether the customer pain is urgent enough.”

“The deck is messy, but there may be a real wedge hidden under weak storytelling.”

“The market narrative is persuasive, but I need to know whether the claimed timing advantage is real.”

This changed the first AI exchange. The model was no longer asked to make the deck look like a memo. It was asked to help expose the burden of judgment.

2. She Split the Work Into Three Zones

Every pitch deck entered three zones.

The Mine Zone

This contained what Maya would not outsource:

- Her investment thesis

- Her appetite for risk

- Her interpretation of founder quality

- Her judgment of whether the opportunity deserved her capital

- Her decision to take a call, pass, invest, or introduce the founder to others

The machine could prepare this zone. It could not own it.

The Shareable Zone

This contained burdens the model could help with:

- Extracting claims from the deck

- Reorganizing information into her structure

- Listing assumptions

- Generating founder questions

- Comparing business model options

- Producing alternative explanations for traction

- Creating a diligence checklist

These tasks widened her field of judgment without replacing it.

The Dangerous Zone

This contained anything that could not be trusted without verification:

- Market size

- Competitor claims

- Customer numbers

- Revenue figures

- Pricing comparisons

- Regulatory assumptions

- Technical feasibility

- Founder background claims

- Fundraising history

- Any statement that might influence a real investment decision

The model was not banned from touching these items. It simply had to mark them as unverified until checked.

3. She Forced Every Claim to Carry a Status

Her old memos had sections. Her new memos had status labels.

Every major statement had to be marked as one of the following:

- Deck claim

- Verified source claim

- Model inference

- Investor hypothesis

- Founder question

- Contradiction

- Rejected or unsupported

This small change restored control.

A deck claim no longer became a fact because it looked neat in a table. A model inference no longer slipped into the memo as if it came from research. An investor hypothesis stayed visibly human. A contradiction was preserved instead of being softened into generic risk language.

The memo became less smooth and more useful.

4. She Used the LLM as a Critic, Not a Judge

In the old workflow, the model often produced a recommendation: strong pass, monitor, take a call, invest only if valuation is attractive.

That felt helpful, but it was the wrong kind of help.

In the new workflow, Maya stopped asking for verdicts. She asked for paths:

- What would make this company fail?

- What assumption does the deck need me to accept?

- What evidence would change my mind?

- What is the strongest skeptical reading?

- What is the strongest charitable reading?

- Which claim deserves the first verification check?

- What question should I ask the founder that cannot be answered with pitch language?

The model became more useful when it stopped pretending to be an investment committee.

5. She Ended With a Human Verdict

At the end of each review, Maya wrote a short human verdict.

Not a machine recommendation. Not a score. Not a polished memo. A decision she could defend.

For example:

“I will take the founder call because the technical wedge may be real, but I do not yet trust the market urgency claim. The call must test customer pain, budget owner, and sales cycle.”

“I will pass because the traction claim depends on pilots that are not yet paid, and the competitive landscape appears stronger than the deck admits.”

“I will not invest now, but I will track the company because the founder’s technical insight is stronger than the current go-to-market plan.”

This was the moment control returned.

The verdict did not ignore the machine. It used the machine. But the commitment had a human name attached to it.

The Situation After Adjoint Thinking

After the shift, Maya did not screen fewer pitches. She screened better.

The local LLM still extracted and reorganized decks. It still saved time. It still helped her prepare for calls. But its output no longer became the hidden architecture of her judgment.

Her new workflow produced several changes.

She trusted the first memo less and used it better.

She became faster at identifying what needed external verification.

She stopped confusing polished deck language with evidence.

She preserved contradictions instead of converting them too early into generic risks.

She asked sharper founder questions.

She passed faster on companies whose story depended on unverified claims.

She took more serious calls with founders whose decks were imperfect but whose pressure points were real.

Most importantly, she knew why she made each decision.

The machine gave her reach. Adjoint Thinking gave her control.

Why Verification Matters in Investment Work

Investment contexts are especially sensitive because a polished answer can influence real capital allocation. U.S. investor protection agencies warn that AI-generated investment information can be inaccurate, incomplete, misleading, false, or outdated.

The technical interest in this area is real. Recent academic work on LLM-assisted startup evaluation explores how multi-agent systems may gather facts, structure arguments, and prioritize startup opportunities. That makes disciplined human oversight more important, not less.

The Angel Investor’s Adjoint Thinking Checklist

Use this checklist when reviewing a pitch deck with an LLM.

Before the LLM

Write the pressure sentence:

“What is the hardest judgment this pitch is asking me to make?”

Then write what must remain yours:

- investment thesis fit

- risk appetite

- founder judgment

- final decision

- willingness to defend the investment or pass

During the First Pass

Ask the model to extract, not conclude.

Use a prompt like:

“Extract the pitch deck claims into my investment review structure. Do not recommend an investment decision. Label each item as deck claim, missing evidence, assumption, or question for verification.”

During Research

Separate sources from synthesis.

Ask:

- What did the deck claim?

- What did external sources support?

- What did external sources contradict?

- What is still unknown?

- What are you inferring?

Before the Founder Call

Generate questions, not verdicts.

Ask:

- What question would expose whether customer pain is real?

- What question would test whether traction is meaningful?

- What question would reveal whether the founder understands the market?

- What question would separate technical depth from technical theater?

Before the Decision

Write the human verdict.

Use this format:

“My current decision is ____. The strongest reason is ____. The weakest assumption is ____. The claim I verified is ____. The claim I do not yet trust is ____. The machine helped by ____. The final judgment is mine because ____.”

Why This Matters

AI can make an angel investor look more disciplined before the discipline is real.

That is the hidden danger.

A prompt template can create structure. A deep reasoning model can create arguments. A local system can protect confidentiality. A research session can produce more material. But none of that guarantees judgment.

Judgment begins when the investor knows what the machine touched, what evidence was checked, what remains uncertain, and what decision still belongs to the human.

This is the problem Adjoint Thinking was written to solve.

If you use AI in work that carries your name, whether that work is a paper, a design, a book, a strategy, or an investment decision, the issue is not only productivity. It is authorship.

The machine can extend your reach. It cannot decide what your capital, reputation, and attention should be loyal to.

FAQ

Can angel investors use AI to review pitch decks?

Yes, angel investors can use AI to extract claims, organize information, generate diligence questions, and compare possible risks. But AI should not replace human investment judgment, external verification, founder conversation, or responsibility for the final decision.

What is the risk of using LLMs for pitch deck analysis?

The main risk is not only hallucination. It is structured overconfidence. An LLM can make a weak or ambiguous pitch look more coherent than it deserves by turning deck claims into polished investment language.

Should an LLM recommend whether to invest?

For serious investing, the safer use is to ask the LLM for questions, assumptions, contradictions, source paths, and risks, not final verdicts. The decision to invest, pass, or continue diligence should remain human.

Why use a local LLM for investor due diligence?

A local LLM may help protect confidentiality when reviewing sensitive pitch decks. But privacy does not solve the judgment problem. Even a private model can still compress, infer, overgeneralize, or make weak claims look structured.

How does Adjoint Thinking help investors?

Adjoint Thinking gives investors a workflow for separating deck claims, verified facts, model inferences, investor hypotheses, contradictions, and final human judgment. It helps AI serve the investment process without becoming the hidden decision-maker.